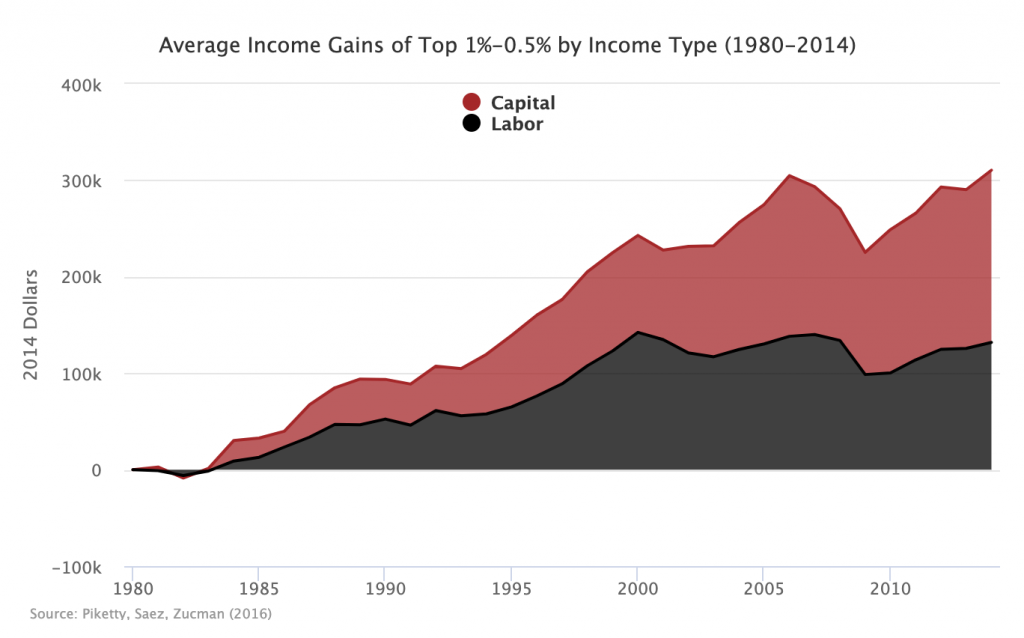

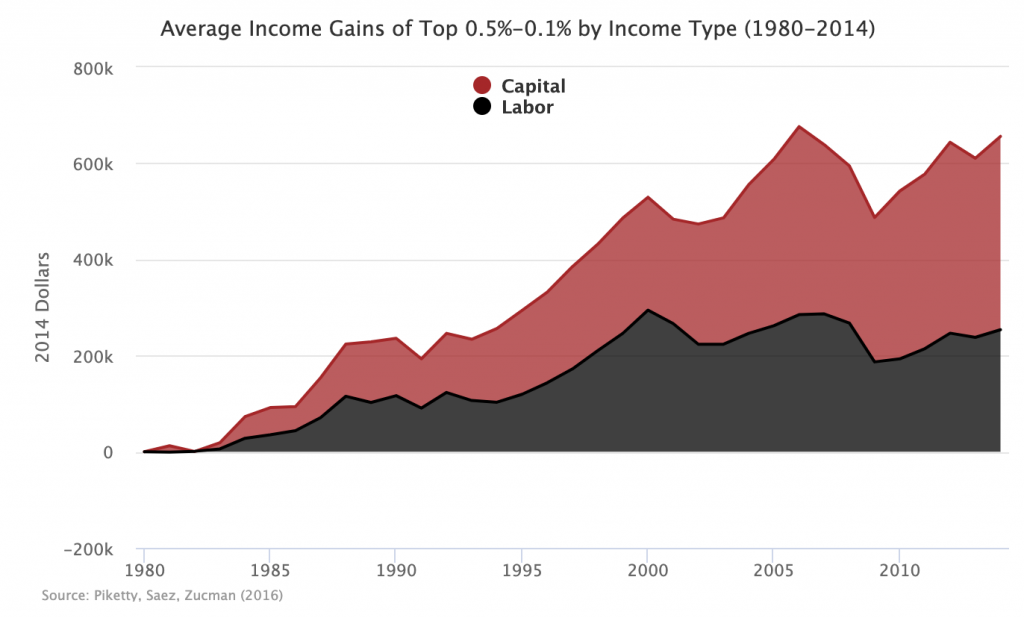

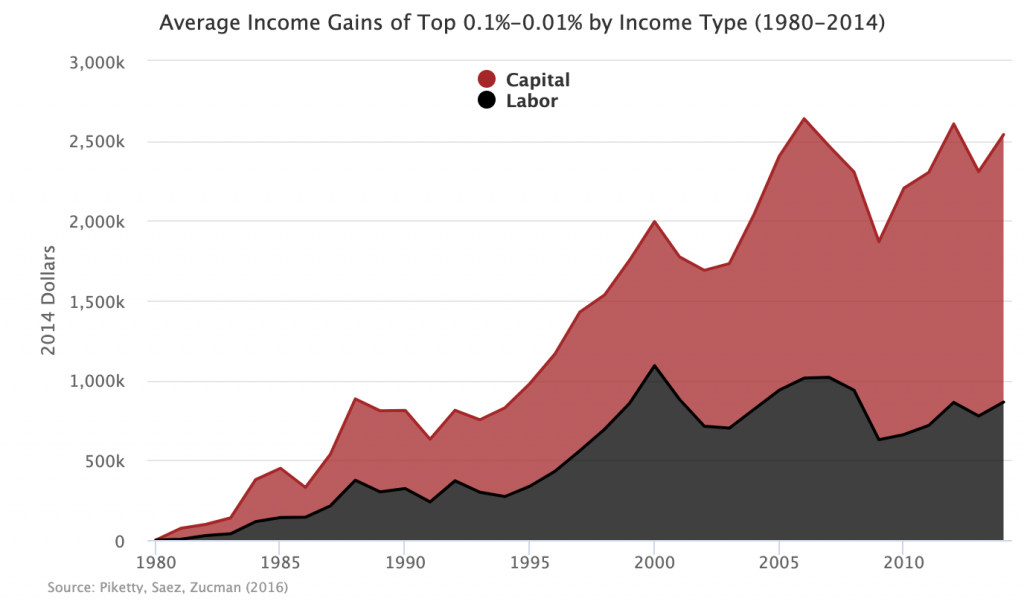

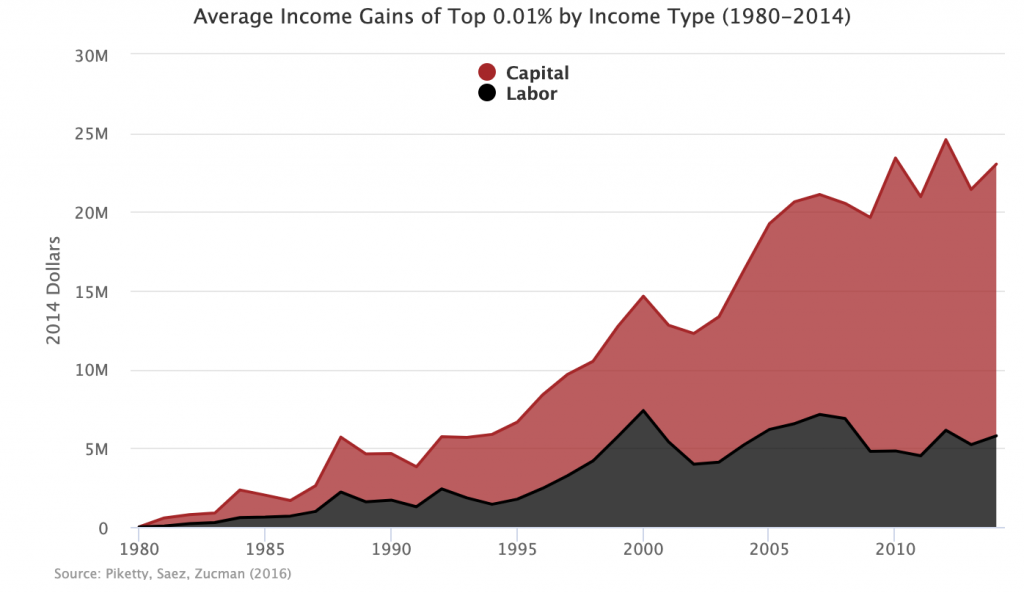

Jonathan Rothwell has a piece in the New York Times that tries to explain why the income of the top one percent has taken off in recent years. David Leonhardt had a similar piece in August. Both Rothwell and Leonhardt cite to Piketty-Saez-Zucman (PSZ) data to substantiate their claims about rising top one percent income, but neither mention that, in the PSZ dataset, all increases in top one percent income since 2000 came from capital income not labor income.

Rothwell's preferred theory for why top incomes have increased so much is that regulations have driven up the labor incomes of a small class of top earners:

Almost all of the growth in top American earners has come from just three economic sectors: professional services, finance and insurance, and health care, groups that tend to benefit from regulatory barriers that shelter them from competition.

But if inflated earnings are the primary cause of top income growth, that should show up in labor income (wages, salaries, the labor component of self-employment income) not in capital income (interest, rents, dividends). Yet when you decompose the top one percent's income into labor and capital components, what you find is that, for the last 14 years, capital income is the sole driver of the income of the top one percent. In fact, labor incomes for the top one percent have actually declined over that period.

What's strange about this omission by Rothwell is that the role of capital in these incomes is noted in the abstract of the very paper Rothwell cites in his piece: "The upsurge of top incomes was first a labor income phenomenon but has mostly been a capital income phenomenon since 2000."

Regulations in the health care, finance, and professional services sectors may be a problem and the top earners in those sectors may be getting a boost from those regulations. But if it is the massive rise of the one percent you are worried about, the source of the problem in recent years seems to lie elsewhere.